The US Open Banking Opportunity

Open banking is coming to America, and that means a new vision for the future of financial services.

The Biden Executive Order on promoting competition contains a number of very interesting provisions. Some of them, such as the initiative to require airlines to refund fees to passengers who get bad wifi or whose baggage is lost, seem unlikely (from my inexpert perspective, at least) to strike a blow against sclerotic corporatism and re-energise late state capitalism to the benefit of all throughout society. On the other hand, some provisions, such as the “right to repair”, might have very significant implications for everything from tractors to iPhones.

The main reason I am interested in the bill, though, it is that is contains a very specific provision on banking that could mean structural change in the US’ financial services sector. This is the provision that calls for the Director of the Consumer Financial Protection Bureau (CFPB) to facilitate the transfer of consumer financial transaction data so consumers can more easily switch between financial institutions and use new and innovative products in ways “consistent with the pro-competition objectives stated in section 1021 of the Dodd-Frank Act”.

(The decade old Dodd-Frank law actually gave consumers the right to access their own financial data but the CFPB has not yet defined that standards that would enable, although it did start the rule making process last year.)

I could not agree more with the economist Tyler Cowen who commented plainly that the portability of bank account information is a good idea. It is an extremely good idea and I am very sympathetic to those (generally more progressive) voices calling for a maximalist interpretation of the data portability provisions. If you could move from one bank to another at the press of a button that would certainly encourage competition.

But how to achieve this? The US has adopted a market-driven approach to the interchange of financial data and this has delivered some great new products and services, but perhaps it is time to push the manufacturers of financial products a bit harder. As Scarlett Sieber noted earlier this year, one of the major causes for confusion in the US has been the lack of open banking regulation that sets specific requirements for banks.

In Europe, there is a clearly defined regulatory framework mandating access to the data banks hold through initiatives like PSD2 and an obvious way forward would be for the US to introduce open banking along such lines, now familiar in many other jurisdictions. That is, the US should mandate that all financial institutions above a certain size implement a common set of APIs with a prescribed set of basic functions so that consumers can give permission to other regulated organisations to have access to their data. This would put US open banking on the same foundations as in the UK, Europe and elsewhere.

The API Opportunity

Banks should respond to this challenge by seeing it as an opportunity to provide new products and services that are not simply a passthrough of the current financial products and services. If we use the simple layering of manufacturing, packaging and distribution of financial services to look at dynamics while assuming that banks want something more than low-margin manufacturing (but will find it hard to compete with distributors as the embedded finance bandwagon rolls on) then we must conclude that they should take packaging seriously.

To do this, they could focus on the APIs themselves and opt to invest in this layer to find new sources of revenue, better returns than pure manufacturing and, and this should not be underestimated, ways to remain relevant to the spectrum of distributors in the new economy. I’ll give an example of this later, but first let us resort to the traditional tool of the jobbing consultant and make a two-by-two matrix.

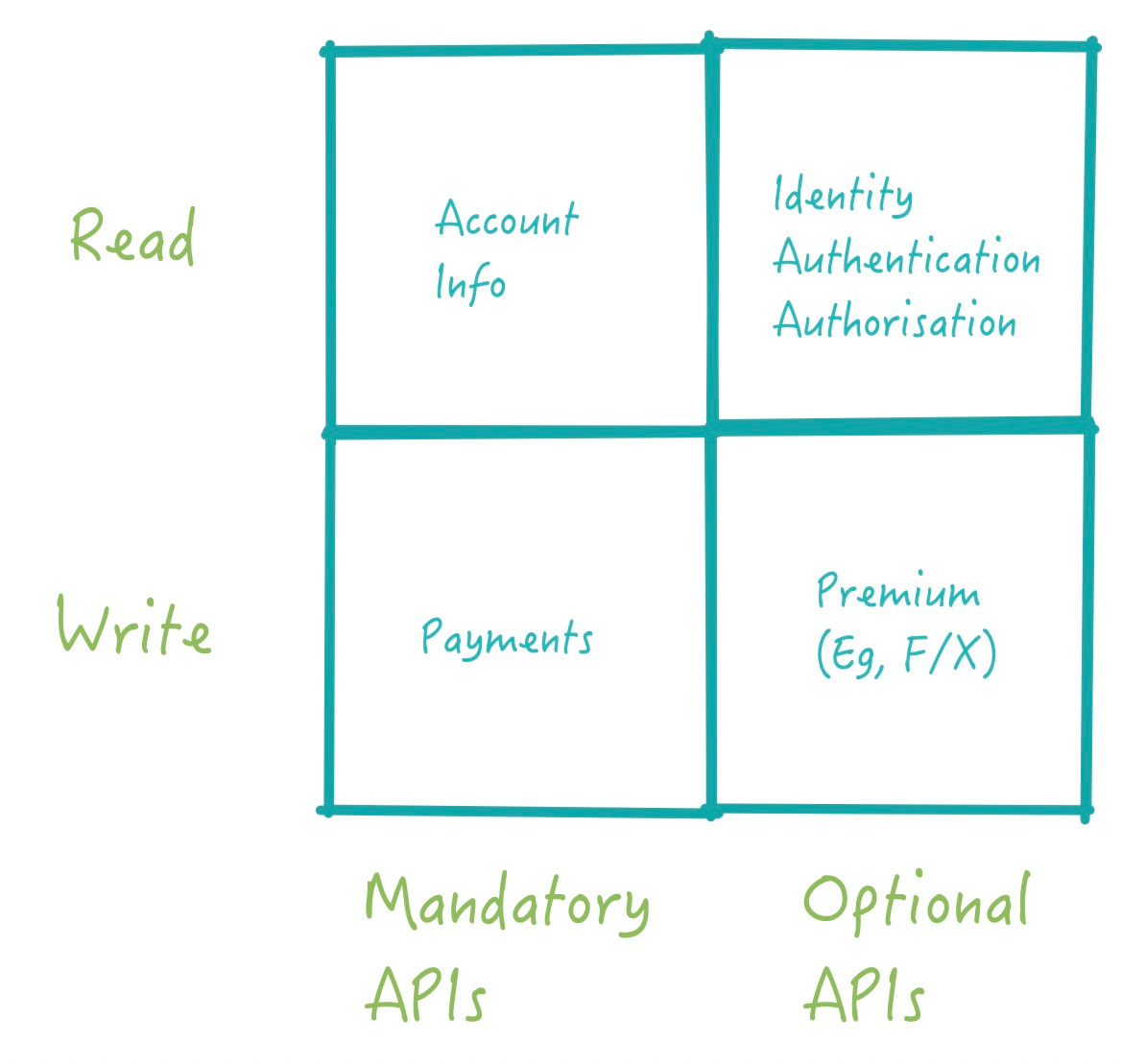

On the horizontal axis we distinguish between the APIs that are mandatory (in a regulated open banking regime, or table stakes in a market-driven regime) and non-mandatory or optional APIs that might be the basis of a more competitive approach.

On the vertical access we distinguish between APIs that are related to making transactions (these are what are generally referred to as "write” APIs) and APIs that are related to information gathering (these are what are generally referred to as "read" APIs).

It doesn't take a very detailed analysis of these quadrants to realise that focusing on the quality and grade of service for the mandatory APIs (in order to make the bank platform more attractive to distributors) makes more sense than trying to invent new ones and then trying to persuade regulators to make them mandatory. When it comes to non-mandatory APIs, on the other hand, it makes sense to invest in creating new APIs that customers will want to the point whether they will even pay for them.

If we focus our efforts on the APIs that relate to information that is not directly related to the financial products, I think we can see the outlines of competitive strategy around those non-mandatory read APIs and an obvious element of that strategy rests on identity, authentication and authorisation services. In other words, a digital identity strategy might provide a means for banks to stay part of transactions in the modern economy.

The UK Lesson

Just to illustrate how the open banking sector might evolve, take a look at the trajectory in the UK, where although only the nine largest banks were required to implement open banking (the “CMA9”, as they are called, because it was the Competition and Markets Authority that set the mandate) there are now more than 70 “account providers” given open banking access to their accounts.

Investment is flowing in. Yapily (who I use almost daily, because they connect my Quickbooks to my bank accounts and credit cards) just raised $51m for European expansion and another of the main open banking “packagers”, TrueLayer raised a $70 million Series D earlier this year. At the time, the CEO of TrueLayer observed that they were redefining how people transact online, saying that “We're building an Open Banking network that brings together payments, data and identity” and (my emphasis).

Incidentally, I note with interest that in the UK what we used to refer to as the non-mandatory APIs have now been labelled "premium" APIs in recognition of the underlying strategic drive. Thus while I agree with the point often made by banks that open banking does not present them with a level playing field (whether they deserve a level playing field or not is another topic entirely), I seems to me that it also presents them with a great opportunities.

Finally, another area where the lessons learned from the UK can be very valuable in America is the scope of the provisions themselves. The UK’s “mid-term” report on “Consumer Priorities for Open Banking” set out just why it is that open banking by itself delivers quite limited benefits for consumers. What is needed is open finance, a view expressed by the US Center for Financial Services Innovation (now the Financial Health Network) in their report on “How Industry Executives View Financial Health”. Again, to use a UK example, open banking is a first step. Nationwide (one of the CMA9) has partnered with another of the packagers, OpenWrks, to pull together information from different accounts and sources to build a more complete picture of the financial circumstances of customers facing financial hardship and therefore find better ways to support them.

American Opportunity

The US should take on board these positive visions in response to the Biden executive order to create a financial sector that takes a more complete view of a customer’s situation and provides services that increase the overall financial health customers. John Pitts, Plaid’s Head of Policy, is well-placed to see the implications here and I strongly agree with his view that the Executive Order adumbrates multi-directional data flow (which creates opportunities, just as we have seen in Europe, for third-party consent managers) and moves the US in the direction of open finance.

This means that financial health providers can obtain a better picture of individuals and their circumstances. They need the raw data to work with. Just as the doctor needs X-rays, bloods and histories, so the AI that powers an effective financial health provider needs your transaction records from your checking account, your mortgage, your pension, your insurers and everywhere else. This is where the connection with open banking, open finance and open data comes from.

The building blocks are in place. The Financial Data Exchange(FDX), a consortium of 200+ members ranging from banks and payment networks through packagers including Plaid and Finicity. The FDX API already has more than 600 data fields in it and these cover not only checking and savings but auto and home loans, investments, pensions, retirement schemes, insurance and so on. With the regulatory clarity that comes from a mandate, access to this data will bring immediate benefits to consumers and innovators alike.

(Don Cardinal from FDX told me that their members see APIs as "the next channel", after online banking and then mobile banking, and I think that’s an interesting description.)

I wrote in Forbes a while ago about the strong narrative that this financial health perspective can provide for a new generation of fintechs: to stop providing financial services and start improving the financial well-being of their customers, to force banks and other manufacturers and to innovate and compete, and to give an accessible vision to the pro-competition drive in the administration.

The Biden administration’s push for open finance is a win for competition and for all competitors.

~

Are you looking for:

A speaker/moderator for your online or in person event?

Written content or contribution for your publication?

A trusted advisor for your company’s board?

Some comment on the latest digital financial services news/media?