The Real World of Consumer Payments

The use of cash is actually going up in the UK.

Dateline: Woking, 16th January 2025.

My life is not that interesting, so I always look forward to the Federal Reserve Bank of Atlanta’s Survey of Consumer Payment Choice. It is an excellent snapshot on the real world of retail payments. In the last survey (June 2024), I was struck by the fact that three-quarters of US consumer have gone mobile with PayPal, Zelle, Venmo and Cash App (a statistically significant increase over the previous survey), and that 70% of consumers made a mobile phone or tablet payment at least once in the preceding 12 months (also a statistically significant increase over the previous year).

The Big Picture

The survey aims to provide a comprehensive understanding of the payment behavior of US consumers. It brings in data from the ground up, bringing together the Survey of Consumer Payment Choice (SCPC) in which consumers report their adoption of payment instruments and the Diary of Consumer Payment Choice (DCPC) in which consumers record details of specific transactions (including dollar values) and their payment choices. Hence the findings are an invaluable picture of what is actually going on, free from fintech hype and crypto campaigning.

The survey reports that 99% of US consumers have a credit, debit or prepaid card. This means that only 1% of US consumers are cardless, whereas 4% of US consumers remain unbanked. Of the US consumers without a bank account, around a third "did not like dealing with banks”, around a quarter said they didn’t write enough cheques to make it worthwhile (it’s the US remember) and a fifth cited reasons related to cost (either a minimum balance required or other charges). That figure hasn’t changed much but the figure that has is the take-up of nonbank payments accounts, now used by almost three-quarters of consumers.

(I find that issue of the unbanked both fascinating and important. As I’ve said more than once, “unbanked” isn’t the problem and maybe banks aren’t the solution. Banks accounts are expensive and inflexible ways to achieve financial inclusion. The basic requirement for participation in the modern economy is not a bank account but a payment account: a way to pay and to get paid. There are many potential providers of such an account. Klarna, for example, has just announced launching an account-like product for deposits and cashback rewards in Europe and America.)

Usage

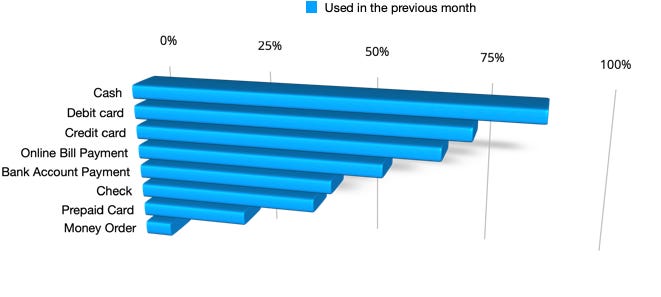

A surprising statistic, for a foreigner like me, comes in the use of payment instruments. When asked which payment instruments they had personally used in the previous month, US consumers responded thus:

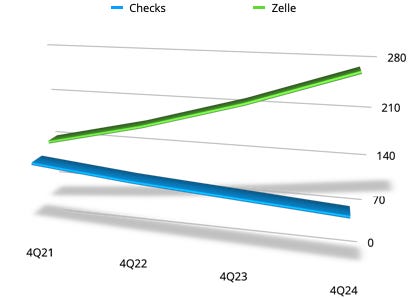

So while account-to-account payments have overtaken cheques, still almost half of all American consumers wrote a cheque in the last month, whereas I couldn’t tell you the last time I wrote a cheque and while I have general idea where a chequebook might be in the house, I haven’t actually seen it for years.

(When I opened a business bank account a few years back, I was presented with a thick book of cheques that I have never touched to this day!)

Account-to-account payments (e.g., Zelle) have overtaken cheques then, but I really want to understand why it is that cheques are still so heavily used. To me, using online bill payment seems so much easier than writing out a cheque, addressing an envelope and mailing it. I remember reading something a few years ago about the float, but the figures don’t seem to support that because the float is so little. Someone else told me it was because of people writing post-dated cheques as a convenience, but surely that is a tiny niche. As far as I can tell, the answer is largely demographic. While just over half of all Americans wrote a cheque last year, those aged 55-64 were the most likely to write a cheque every month while almost half of those in the 18-24 wrote no cheques at all.

Surprise

The extensive use of cheques was not the most surprising statistic in the survey as far as I was concerned. That was the statistic about cash. In the 2019 survey, the average amount of cash a U.S. consumer held in his or her pocket, purse, or wallet was $60 (the median was $24). That rose substantially in 2020, presumably because of the pandemic, reaching $76, and then climbed again to $81 in 2023. Almost four-fifths of consumers carried at least $1 at the beginning of at least one of their diary days. I am carrying no cash today and won’t tomorrow either. Nor do I carry any when I went into London this week and nor will I carry any when I head to Switzerland next week.

(It seems that Americans are now heading in the same direction. According to Marqeta’s 2024 State of Payments report, nearly three-quarters of U.S. consumers aren’t concerned about moving towards a cashless society. In fact, more than a quarter of respondents said it feels awkward to pay with cash, with nearly half of those ages 18 to 34 expressing this sentiment.)

with kind permission of Helen Holmes (CC-BY-ND 4.0)

In the UK, as in most developed countries, the use of cash in shops is generally falling, although it has actually risen slightly in the UK over the last three years. The British Retail Consortium (BRC) has recently published its annual Payments Survey, showing that while debit cards remained far and away the most common method of payment (two thirds of all UK retail spending) there was a rise in the use of cash for the second year in a row to 19.9% of transactions in 2023 (from 18.8% in 2022).

The usual explanation for this is that in times of economic hardship, people find it easier to budget with cash, and that may well be true. It may also be true, however, that in difficult times more spending finds its way into the grey economy, a topic I saw raised in an online discussion recently where someone was complaining about NatWest asking them questions when they went to withdraw £8,000 in cash in order to pay their builder.

In summary, the overall amount of cash “in circulation” continues to rise. According to Nationwide, the biggest increase in cash withdrawals was recorded in Chiswick, West London (up 140%). Quite why the people of Chiswick are such enthusiastic users of cash is not clear to me at all (and the statistics do not show whether the bulk of these withdrawals are during the day or late at night) but I’m keen to learn from any local residents. Is this cash actually going in to circulation as grease in the cogs of less formal sectors of the economy, or is it not in circulation at all and stuffed under the mattresses of drug dealers?

Are you looking for:

A speaker/moderator for your online or in person event?

Written content or contribution for your publication?

A trusted advisor for your company’s board?

Some comment on the latest digital financial services news/media?