Cards Cost… Someone

There's no such thing as a free lunch, or free miles.

Dateline: New York, 31st October 2022.

The Economist magazine ran an article — provocatively entitled “Can the Visa-Mastercard duopoly be broken” — that began by pointing out just how much the current retail payments infrastructure costs to use. The focus was on the cost of cards. Merchants are not happy about the fact that over the last decade the fees that they pay to accept cards have doubled — to $138 billion in 2021, according to the Nilson Report — which makes them, according the National Retail Federation (NRF), the second highest operating cost after the cost of labour. The overall costs, according to The Economist, are such that the current payment system adds 1.4% to retail prices.

A New York Diner’s view (October 2022).

A “Durbin 2” bill is being proposed in the USA to limit these fees. American banks are naturally lobbying strongly against any kind of price-fixing, arguing that an interchange fee cap is simply a forced transfer of cash from banks to retailers.

(The global evidence on such topics broadly supports this view, by the way.)

The banks also argue that any such cap would “decimate card rewards programs, such as airline miles, valued by American families.”

(The global evidence on such topics broadly supports this too, by the way.)

Is that a bad outcome though? The dynamics of the credit card rewards world are somewhat perverse. Matt Stoller points out (in BIG, his newsletter on the politics of monopoly power) that credit card reward schemes deliver some $20 billion per annum in America and most of this goes to high-income households. In essence the poorest households pay $21 each year to fund these schemes and richest households earn $750 every year.

In economic terms, what this means is that credit card issuers make a lot of money and pass enough of it back to cardholders to create “switching costs” that are a barrier to competition.

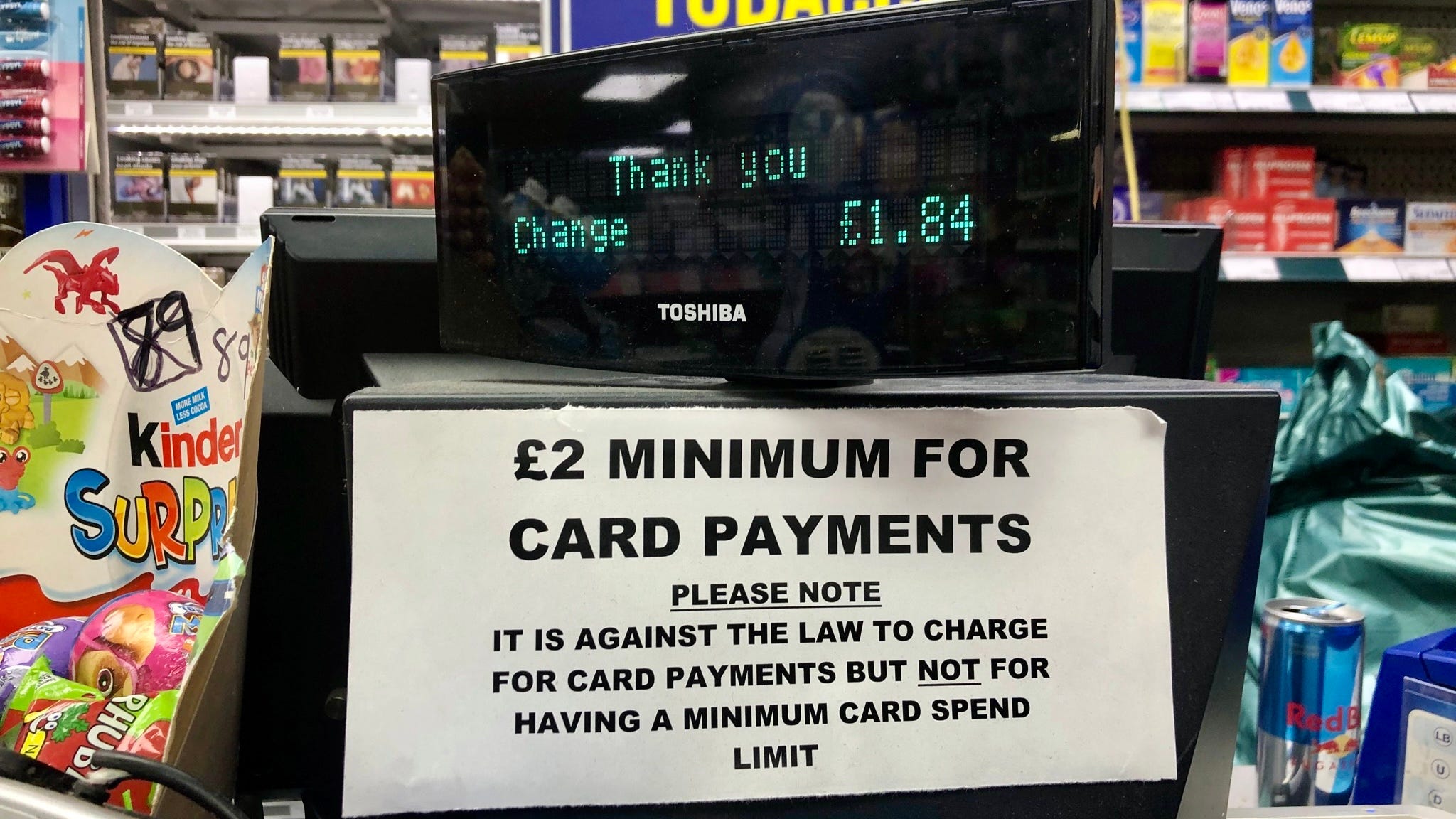

Here in the UK we have a similar problem, although fees are lower. This is why I use my premium card to buy everything from cups of coffee to furniture, meaning that merchants pay the maximum charges and I earn the maximum rewards. In this I am no different to many other well-off people, such as the journalist Jaci Stephen who wrote in a UK newspaper that “my miles cost me nothing” without reflecting on the fact that they must cost somebody something since airlines are not charities.

That somebody is, of course, the poor shopper trapped in the cash economy.

The inevitable consequence of stopping retailers from surcharging for cards is to raise prices and transfer money from the less well-off to the better off. Canada, where consumers are absolutely addicted to rewards, is a good case study. Canadians “get their points, their rebates, their benefits… but they rarely ask themselves who's paying for that”.

The fact is that there is a fundamental conundrum in the surcharge debate which is that consumers want the points and frequent flier miles that come with credit card use, but they don’t want to be surcharged to pay for it. Without surcharges, the people who pay with cash or debit cards are subsidising my frequent flier miles and gift vouchers.

The dynamic is clear: the more rewards that credit card issuers provide, the more expensive they are for merchants to accept.

There are ways for merchants to bypass the cards and rewards nexus and offer their own rewards directly to the consumers rather than paying for banks to provide rewards to the customers. Indeed, the duopoly article quotes the correspondent being incentivised by an online retailer to use an app linked to her bank account (via Plaid) to pay directly through the banking network rather than use a card.

You can see the attraction from the merchant perspective so one might expect these schemes to grow. I have said more than once that these bank account payment alternatives will grow through the use of retailers apps rather than as card replacements and in a way I am surprised that more retailers haven’t already gone down this route.

Practical Steps

Back to the main issue of payment costs. There are, and have always been, only two ways to get costs down: competition or regulation. When it comes to competition, the landscape is certainly changing.

For one thing, when the card schemes were created, there was no universal network, linking all consumers, all merchants, and all banks, so it was necessary for the banks to create what became the Visa and MasterCard networks. Now, however, there are networks in place that connect everybody all the time, and so there is no need to use those private networks anymore. All around the world we can see payment networks growing up that use ubiquitous, mobile networks to reach consumers and merchants, ubiquitous broadband networks to connect together financial institutions, and in many cases, the beginnings of the regulatory separation between banking and payments.

Inventive new approaches are all around us. Merchants already have options such as “buy-now-pay-later” (BNPL) available to them, and of course they could always use cryptocurrencies now or perhaps central bank digital currencies (CBDCs) in the future, neither of which use bank networks to effect transactions.

Hey, Hey A2A

It seems to me, however, that despite BNPL and CBDC, for the foreseeable future the serious mainstream competition is going to be from account-to-account (A2A) schemes that transfer money between consumers and retailers through the instant payment networks.

(Hence I was interested to see that The Clearing House is launching a “pay-by-bank-account” scheme to provide an alternative to cards for bill payments — and other recurring payment use cases — where the protections inherent in (and costs of) card payments are not justified.)

In the UK the Payment System Regulator (PSR) has included in its plans for 2022/23 the removal of barriers to the uptake of A2A retail payments, which it says can provide a “credible" alternative to card schemes. As part of these plans it intends to investigate whether the commercial incentives for banks, intermediaries and merchants are there to support greater use of A2A payments and to see what it can do to increase uptake and promote competition with cards.

The PSR is also working with the Financial Conduct Authority (FCA), the Competition and Markets Authority (CMA) and the Treasury on the future of open banking regulation, which will play a major role in A2A payments uptake, and is setting up a strategic working group on A2A with them. They have identified four key issues that will need to be addressed to accelerate A2A use in retail. These are:

Overall functional capability: The PSR talk about the need to address the particular user needs of retail purchase transactions such as retailers’ ability to trigger the payment with the customer’s consent when the customer is not present. My view is that interoperable request-to-pay (R2P) services will take care of the “customer is present” transactions, whether in the contactless tap-and-pay retail environment or online, and interoperable variable-recurring-payment (VRP) services will take care of the “customer was present” situations needed to replace direct debits.

Practical dispute processes: Retail transactions bring new risks, such as unsatisfactory goods being delivered after the payment, or the retailer not acting in good faith. Consumers are used to, and like, the protections afforded by card products so, as we will discuss in more detail below, the industry needs a strategy to deliver appropriate levels of protection for A2A transfer.

Widespread access and appropriate reliability: Retailers and consumers must be able use their preferred payment method when they want to. They want to ensure that the system works properly and that customers don’t have any problems when they make their purchase. They also want to explore what the seller needs to feel assured that they will be paid, and ensure that there is sufficient capacity to match the potential uptake in the future. There are several ways to achieve access and reliability, of course, but my general feeling is that building a parallel digital currency infrastructure of instant device-to-device (as opposed to account-to-account) value transfer is the best solution.

A sustainable funding model: For A2A payments to work in retail, there must be commercial model that ensures all parties receive sufficient compensation for the services they provide, and can continue to invest in new products and further innovation. I think it is generally recognised that the models are increasingly unlikely to be based purely on transaction fees.

As part of the PSR’s plans for 2022/23 it therefore intends to look at these issues and see whether the commercial incentives for banks, intermediaries and merchants are there to support greater use of A2A payments and to see what the regulator can do to increase uptake and promote competition with cards.

It will not happen overnight, of course, but for many of the payment transactions that will generate volumes in the app-driven, smartphone-centric, always-on economy the merchants’ drive to reduce costs will begin to have an impact on the payments mix we are familiar with today. This is because even with no chargeback mechanism, people like me will happily give Amazon access to their bank account in return for three months’ free Prime or give Tesco access to their bank account in return for double club card points.

Would I give Air Ruritania access? No, of course not, I’d use my credit cards for that, as I would for all potentially risky transactions, and I’d happily pay the surcharge!

Are you looking for:

A speaker/moderator for your online or in person event?

Written content or contribution for your publication?

A trusted advisor for your company’s board?

Some comment on the latest digital financial services news/media?